Buy or Rent a house?

Generally, people say that instead of paying rent for a property, it is better to take a loan and buy that property and pay EMIs instead of rent. But is it really that easy? Think.

Vidyasagar

11/1/20245 min read

Should I buy or rent a house?

Generally, people say that instead of paying rent for a property, it is better to take a loan and buy that property and pay EMIs instead of rent. But is it really that easy? Think.

Why pay rent and give money to a property owner if you can afford to buy a property? Many suggest an alternative approach: buy a property with a 20% down payment, finance it with a mortgage, and then rent it out to cover the monthly EMIs. In this scenario, the rental income covers your EMI payments, making it seem like the property is "paying for itself." Over time, you may feel like a savvy investor—believing that your property’s value is appreciating, you’re not paying EMIs out-of-pocket, and, after 20-25 years, the property will be yours without much personal expense.

But how realistic is this?

This idea is often encouraged by well-meaning family members—parents, in-laws, or even a spouse—who view property as a safe investment. However, the reality is more complex. Consider factors like rental market fluctuations, property maintenance costs, vacancy risks, and mortgage interest over the loan term. Additionally, the appreciation of property values isn’t guaranteed, and, in some cases, your net profit may not be as high as anticipated.

So, while this strategy sounds appealing, it’s important to carefully evaluate whether it will genuinely achieve the financial freedom and returns you envision.

Does this strategy really work as intended? Can rental income consistently cover EMI expenses? The short answer: it's complicated.

Typically, rental yields are lower than the EMI costs. If you come across a property where the rent truly covers the entire EMI, stop reading this and buy that property immediately—and don’t forget to call me right after! But in most cases, the rent will fall short of the EMI, meaning you'll need to contribute additional money each month.

Additionally, rental yields in many areas are modest, usually hovering around 2-3% annually, while mortgage rates often range much higher around 8.5%. This gap means that, unless the property appreciates significantly over time, the “self-paying property” idea may fall short of expectations.

Before diving into the details, let’s first understand the concept of rental yield. Simply put, rental yield is the return on investment you earn from renting out a property, expressed as a percentage of the property's value. For example, if a property is valued at 1 crore and generates 2 lakhs per year in rental income, the rental yield would be 2%.

Understand EMI

Which means, Equated Monthly Instalments. where one pays a fixed amount of money every month to repay the loan. Which includes interest on the principal amount and little portion of the remaining principal amount.

Now, guess how much one has to pay as an EMI or how much percentage of the principal amount has to be paid every month or year to repay the loan amount. It’s close to 10% of the total cost of the loan amount.

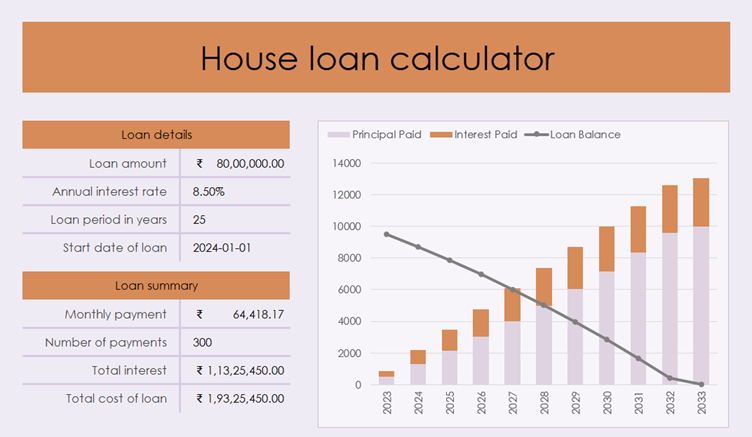

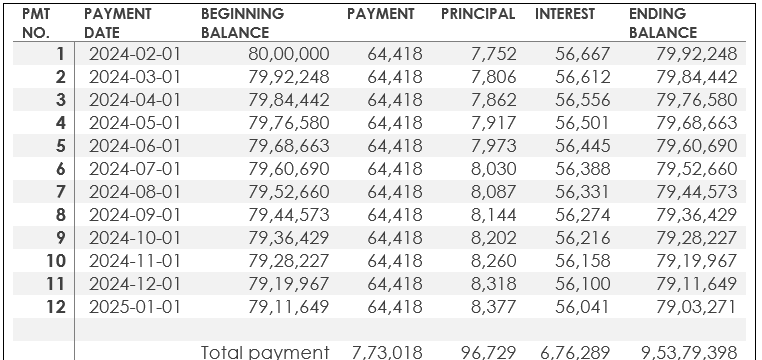

In the above illustration, consider a property worth 1 crore, and 20 lakhs has been paid as down payment and remaining 80 lakhs has been sourced as loan from a bank with an interest rate 8.5% pa, for the period of 25 years.

Monthly EMI is 64500, multiplied by 12 equals to 7,74,000 per year. For the above same property rental yield is simply 25000 to 30000 per month which is roughly 3 to 3.6 lakhs per annum. Which make the rental yield 3.5% per annum.

now, 7,74,000/80,00,000 make up 9.675% of EMI per year. Compare the rental yield vs EMI. It’s 3.5% vs 9.675% pa.

Let’s breakup the EMI.

Bank interest rate is 8.5% but then why EMI is 9.675%. If only interest of 8.5% is paid, then the principal amount will never decrease. EMI has 2 constituents. Interest part and principal amount part. Interest amount is 8.5% of remaining principal amount. And another extra 1.175% is to reduce your principal amount.

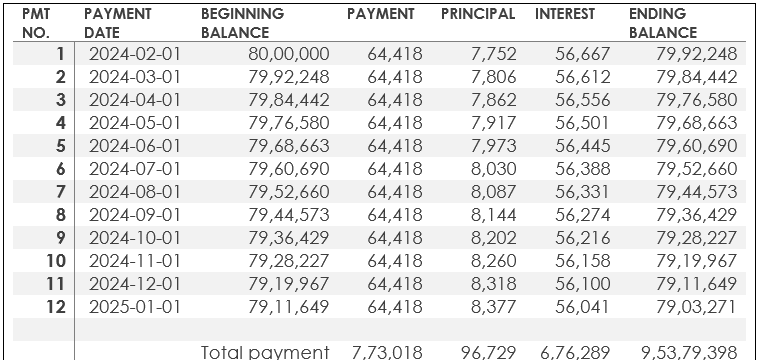

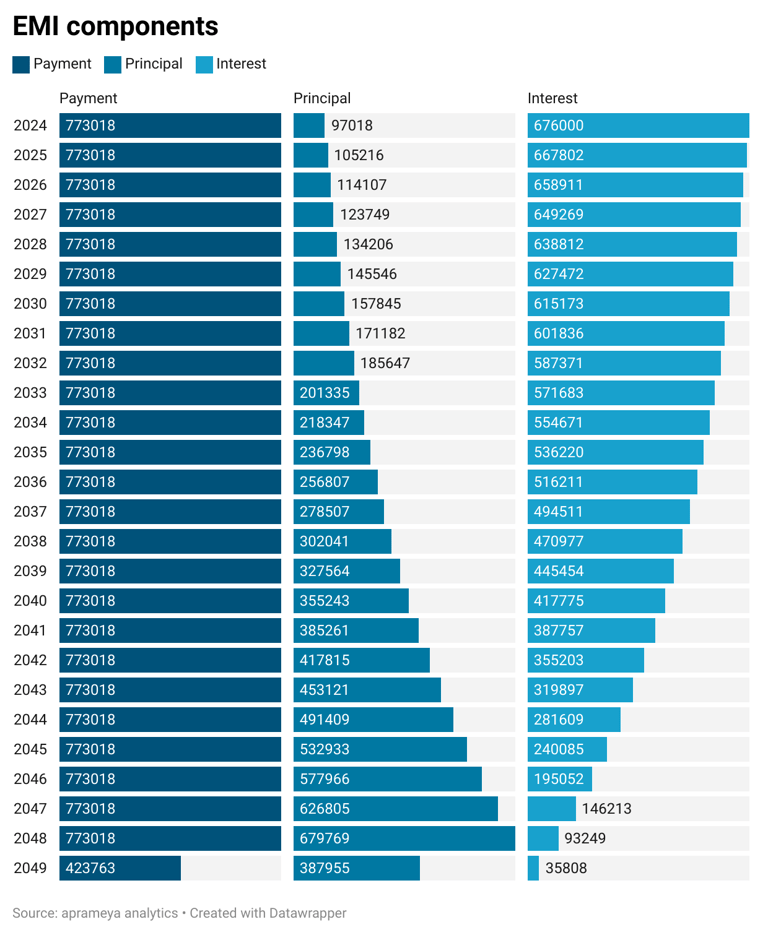

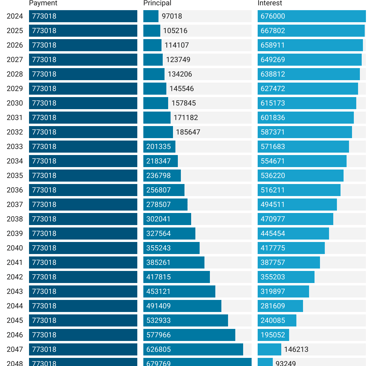

Consider the table above, after one year remaining principal amount is 79,11,649, while the total amount paid in the year is 7,73,018. Majority of which is covered by interest payments, which amounts to 6,76,289 which is 8.5% of EMI. Principal amount paid is 96,729, which is 1.125% of total EMI for year.

Now in the second year, interest will be calculated on the remaining principal amount. Now compare the first year EMI with 2nd year, and check the difference. The total amount of EMI paid remain same, the amount of interest paid in second year is lesser than the first year, and principal amount paid is more than the first year.

So renting is good, isn’t it? Hmm arguable!

So one thinks that renting a property is better than investing in the property, well not exactly. It’s upto the individual’s goal, lifestyle, risk, income and various other factors. One good reason is that though the amount of money paid as rent increases year on year by 5%, but EMI doesn’t. EMI is flat through out the loan cycle. Maybe it changes by more or less by 1-2% as per RBI’s policy, but make sure to increase your EMI amount rather than increasing the time to repay. And most important thing is the value of asset appreciates as time goes by.

It's purely personal choice

There are various factors affect the decision to buy a home or rent a home. Some chose to stay in rent for 10 years and enjoy the lifestyle and some prefer to invest in high yielding asset like equity or mutual funds, which is a smart decision too. In my opinion investing early in equity markets helps compounding your wealth at a faster rate. That’s entirely a huge topic to be discussed.

Then how can I allocate funds and capital to invest? Can I get rental income by buying a property by paying full amount or should prefer loan? Which is better? Which way is better to reap maximum benefits of every single rupee?

Tune in for more from Aprameya!